June 10, 2026

What is Payment Orchestration? A 2026 guide for payments leaders

- TL;DR

- What is payment orchestration?

- The five jobs of a payment orchestration platform

- How does payment orchestration work?

- Payment orchestrator vs payment gateway vs PSP

- The three conditions that break a single-PSP setup

- Payment orchestration: new sources of revenue

- When do you need payment orchestration?

- What payment orchestration does not solve

- Multi-tenant vs dedicated instance: the architecture trade-off most buyers miss

- How much does payment orchestration cost?

- Is payment orchestration PCI compliant?

- Where payment orchestration is heading next

- Frequently asked questions

- Is a payment orchestrator the same as a payment gateway?

- Is a payment orchestrator the same as a PSP?

- Do I need to replace my existing PSPs to use payment orchestration?

- How many providers do I need before payment orchestration makes sense?

- Can payment orchestration help with recurring payments and subscriptions?

- What is the difference between multi-tenant and dedicated instance payment orchestration?

Last updated May 21st 2026

Around half of online merchants now use more than one payment provider. That shift, more than any other in the last five years, is what created the category called payment orchestration and the technology layer at the center of it. The term is still used loosely. People confuse payment orchestration with a gateway, ask whether it replaces a PSP, and want to know what actually changes inside a business the day a payment orchestrator goes live. Below, the answers in the order a payments leader asks them.

TL;DR

- Payment orchestration is a technology layer that connects multiple PSPs, acquirers, and payment methods through a single integration, routing every transaction to the provider best suited to handle it.

- It typically lifts authorization rates by 2 to 3 percentage points, reduces processing costs, and removes months of engineering work when adding new payment methods or markets.

- The case for payment orchestration sharpens once a business is processing roughly $1M per month, selling into two or more countries, or using two or more PSPs.

- Gr4vy is the only payment orchestration platform built on dedicated single-tenant cloud instances with edge localization capabilities. Unlike shared SaaS environments, every merchant operates on its own isolated infrastructure, deployed in-region to support performance, resiliency, and regulatory requirements. This Infrastructure-as-a-Service model enables data localization for markets where payment data cannot leave the country, helping enterprises meet strict sovereignty and compliance mandates without sacrificing flexibility or scale.

What is payment orchestration?

A payment orchestrator is the software layer that sits between your checkout and every payment provider you use, process each transaction, decides which provider should handle it, sends it on, and brings the result back. The customer sees a single checkout. Your team sees one dashboard. The complexity of multiple PSPs, acquirers, payment methods, and fraud tools is absorbed inside the orchestration layer.

A payment orchestrator does not authorize payments, move money, or own a merchant account. Its role is to coordinate the providers that do, deciding which one is best suited to each individual payment based on rules you set and conditions it sees in real time.

That distinction matters commercially. A PSP earns more when more transactions flow through its own pipes. Payment orchestration earns nothing from routing one provider over another, which is why a well-designed orchestrator can route transactions away from underperforming providers without any conflict of interest. The neutrality is the product.

The five jobs of a payment orchestration platform

Payment orchestration handles five jobs across every transaction.

It processes the transaction request from your checkout and applies any pre-routing logic you have configured (3D Secure, fraud screening, business rules).

It routes the transaction to the optimal provider based on cost, expected approval rate, geography, card BIN, provider uptime, or any combination of criteria your team specifies.

It handles failover when a provider returns a soft decline or times out, attempting the transaction through a backup provider before the customer sees a failure.

It stores payment credentials in a provider-agnostic Vault, so tokens work across every connected PSP and customers do not have to re-enter details when you switch or add providers.

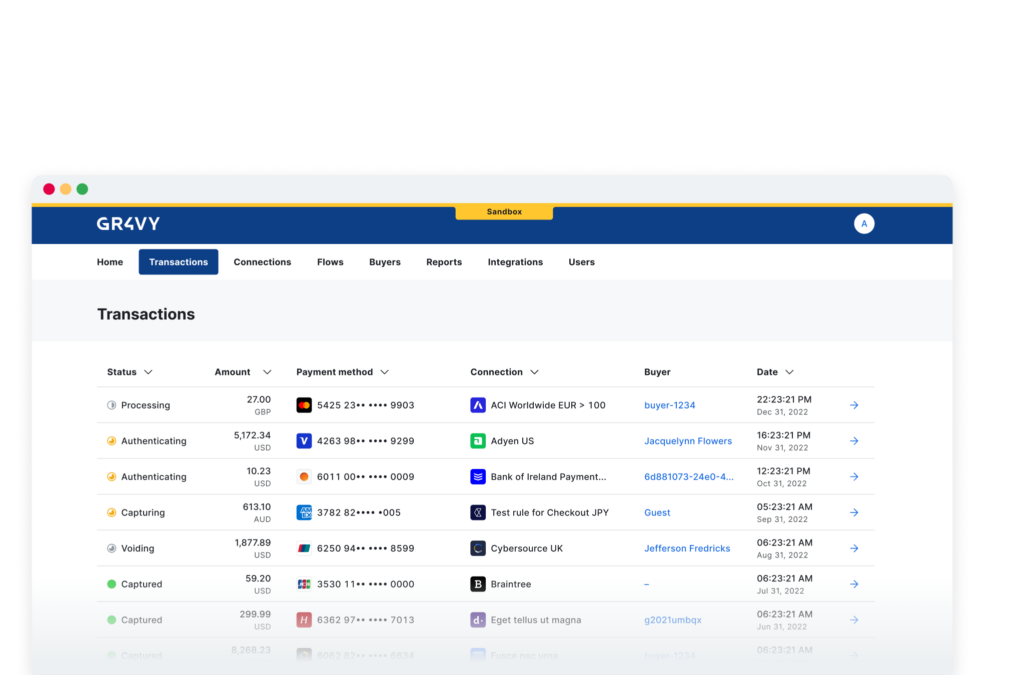

It consolidates reporting across every provider into a single dashboard: settlements, fees, decline reasons, chargebacks, refunds, all attributable to provider, market, payment method, or card type.

Each capability is useful on its own. They become substantially more useful as a coherent system, which is the point of choosing a serious platform rather than assembling the equivalent yourself.

How does payment orchestration work?

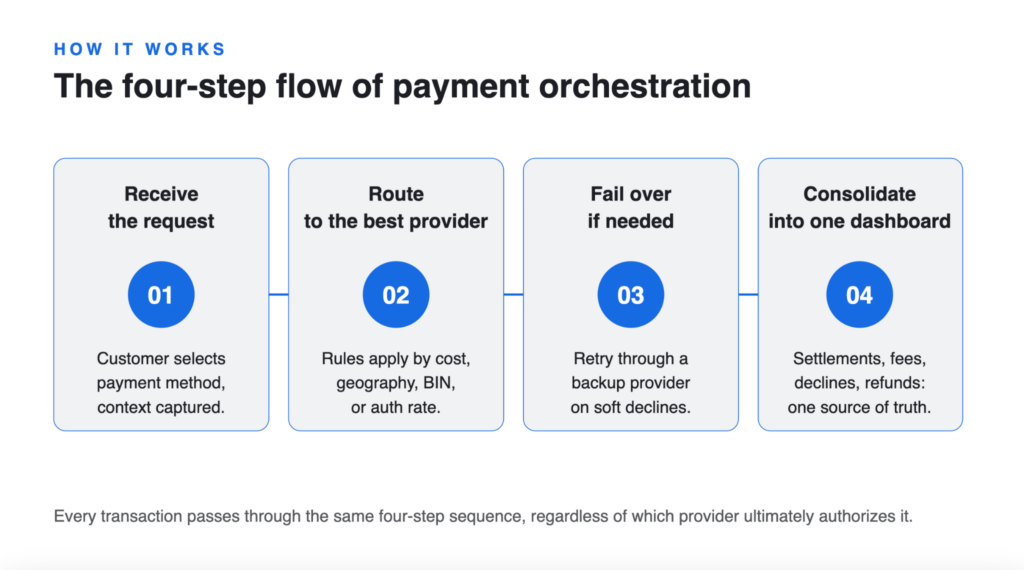

Walk through what happens between a customer clicking “pay” and a settlement appearing in your finance dashboard.

The customer reaches checkout and selects a payment method. The payment orchestration layer receives that selection along with contextual information: country, currency, basket value, card BIN if relevant. Before deciding anything else, the merchant decides which payment methods to show the customer in the first place, because the right methods depend on the customer’s market. A shopper in São Paulo expects Pix. A shopper in Amsterdam expects iDEAL. Showing the wrong set of methods is itself a leading cause of checkout abandonment.

Once the method is selected, the payment orchestration platform applies your pre-routing logic. This usually includes 3D Secure rules, fraud screening, and any business-level constraints. The platform then evaluates which provider should handle the transaction as per the merchant setup, sends it there, and waits for the response.

If the transaction succeeds, authorization and settlement proceed through the chosen provider in the normal way. If it fails, payment orchestration can attempt the transaction through an alternative provider before returning a decline. This failover mechanism is the single capability most directly responsible for recovered revenue.

All transaction data, regardless of which provider ultimately handled the payment, flows back to the orchestration dashboard. Your finance team sees a single source of truth.

Payment orchestrator vs payment gateway vs PSP

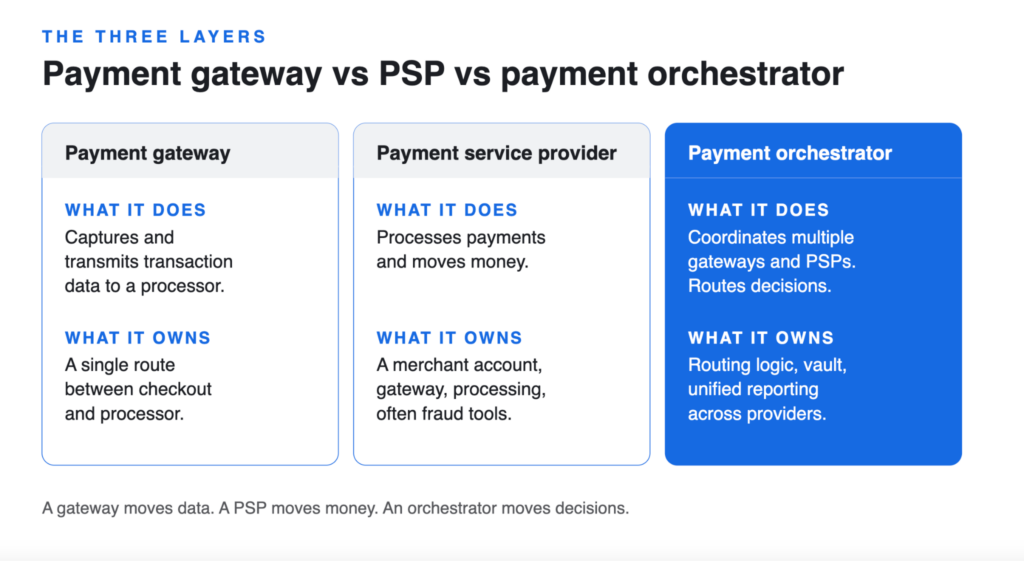

The three layers are often confused. The cleanest mental model is this: a gateway moves data, a PSP moves money, an orchestrator moves decisions.

| Capability | Payment gateway | PSP | Payment orchestrator |

|---|---|---|---|

| Connects to multiple providers | Yes | No | Yes |

| Single API integration | Per provider | Single provider | Yes, across all providers |

| Intelligent routing across providers | No | Limited to internal options | Yes |

| Automatic failover | Yes | No | Yes |

| Centralized reporting across providers | No | No | Yes |

| Provider-agnostic tokenization | No | No | Yes |

| Switch providers without re-integration | No | No | Yes |

| Owns merchant account | No | Yes | No |

| Processes payments directly | No | Yes | No |

A payment gateway captures payment information from the checkout, encrypts it, and transmits it to a processor or acquirer for authorization. It does not decide which provider to use. It follows a predetermined path.

A payment service provider (PSP) is a bundled solution combining gateway functionality, a merchant account, payment processing, and often fraud protection and reporting. You get an integrated stack from a single vendor, and you cannot optimize across providers because you only have one.

A payment orchestrator sits above gateways and PSPs and coordinates between them. It connects to multiple providers through a single API and routes each transaction to the optimal destination based on the rules you set. For a deeper breakdown, see payment orchestration vs payment gateway vs payment processor.

The three conditions that break a single-PSP setup

A single-PSP setup is the right answer for many businesses. It only stops working when one of three things happens.

Geographic expansion. A PSP that performs well in one market may have weaker acquiring relationships, slower decline recovery, or no native support for local payment methods elsewhere. Merchants entering Brazil, India, or the Nordics quickly find that the provider that served them well at home is not the right answer in those markets.

Scale. As volume grows, the gap between a good authorization rate and a great one converts into seven-figure numbers. A merchant processing $200 million a year cannot afford to ignore a two-point approval-rate gap between providers, even if both are technically functional.

Operational drag from multiple providers. Many merchants reach a multi-PSP setup organically, adding a second provider for redundancy or a third for a new market. Each integration was a reasonable choice in isolation. Taken together, they create fragmentation: different APIs, different reconciliation timelines, different reporting formats, different ways of representing a chargeback. Finance teams stitch together exports at month-end. Engineering teams maintain integrations whose original authors have left the company.

This is the situation payment orchestration resolves. Everything runs on the same rules and shows up in the same dashboard.

Payment orchestration: new sources of revenue

The business case for payment orchestration is more than productivity.

Higher authorization rates. Routing each transaction to the provider most likely to approve it lifts authorization rates by two to three percentage points in most deployments, with more fragmented multi-PSP estates seeing larger gains. Within four months of moving to a dual-acquirer setup, Australian retailer Baby Bunting measured a 2.8% authorization uplift that contributed to record online sales above $120 million. On $100 million of annual volume, a single percentage point of recovered approvals is roughly $1M of revenue, recovered without any change in customer acquisition spend. On $500 million it is $5M. At enterprise scale, two or three points of authorization uplift is a strategic line item.

Lower processing costs. Smart routing sends each transaction to the lowest-cost provider that can authorize it, which compounds across millions of transactions. Local acquirers in each market reduce cross-border fees and FX leakage. Mattilda, a Latin American education payments platform, posted a 60% reduction in payment costs after consolidating collections across multiple acquirers this way. For platform businesses, the cost reduction story is often as significant as the revenue uplift.

Faster speed to market. Adding a new payment method or a new market used to mean months of engineering. With a coordinating layer above the providers, both become configuration changes in a dashboard. A platform with hundreds of pre-built provider connections can enable a new local payment method in days.

Reduced engineering overhead. Engineering capacity that used to maintain three or four PSP integrations gets returned to product work. This is consistently the orchestration benefit engineering leaders rate highest when asked retrospectively, partly because it shows up as work that no longer happens.

Recovered revenue from failed payments. Failover, dynamic retries, Network Tokens, and Account Updater each recover transactions that single-PSP setups would lose. Industry research puts the recoverable share of failed-payment revenue as high as 14%, depending on the merchant’s profile.

Unified reporting. Two thirds of multi-PSP merchants lack a unified view across providers. Roughly 30% of payment failures go unresolved because of the resulting visibility gap. Reconciliation, fee analysis, and provider benchmarking all become possible the moment data from every provider runs through one platform.

When do you need payment orchestration?

The answer comes from the setup, not from the size. A subscription business doing modest monthly volume across five countries faces the same fragmentation, the same provider-specific approval-rate variance, and the same reconciliation overhead as a much larger single-market merchant. The smaller business often needs orchestration sooner, because the complexity is already there.

The case sharpens whenever any of three conditions appears: a second market, a second PSP, or a meaningful approval-rate gap between regions. Larger volume amplifies the return on every percentage point of recovered approvals, but it does not gate access to the underlying benefits. Smaller merchants with the right setup capture them too.

Beyond volume, the conditions that consistently signal a payment orchestration-shaped problem are these. Multiple providers already in the stack, particularly across regions. Cross-border operations where approval rates vary noticeably by market. Subscription or recurring billing exposing the business to involuntary churn. Concerns about vendor lock-in, particularly where switching PSPs is a multi-quarter migration.

There are conditions where payment orchestration is not the right move yet. A single PSP, single market, single payment method, and modest volume. No one to own payments operations. A platform replatforming that needs to finish first.

The threshold is not a fixed number. The right question is whether multiple providers, multiple markets, or multiple payment methods are already creating operational drag, or will within twelve months.

What payment orchestration does not solve

The vendor pitch for payment orchestration tends to be uniformly positive. The reality is more mixed, and most failed implementations come from underestimating four things.

It does not negotiate your PSP contracts for you. Routing transactions across multiple providers gives you leverage, but the leverage only converts into better rates if someone uses it. Merchants who add an orchestration layer without then renegotiating PSP terms typically leave the largest portion of available savings on the table. The orchestrator hands you the data and the optionality. Acting on both is still a job.

It does not eliminate the need for someone to own payments. A payment orchestration platform replaces engineering work with configuration work, which is much faster but not zero. Routing rules need to be defined, tested, and revisited. Provider performance needs to be reviewed. New payment methods need to be activated and monitored. Businesses that bought into orchestration expecting it to run itself usually end up with a powerful platform that nobody is steering.

It does not fix a checkout that has other problems. If the checkout itself has friction unrelated to payment routing, broken mobile flows, missing local payment methods that exist in the orchestrator but were never enabled, or a confusing form layout, the orchestration layer will not solve those problems. A 30% checkout abandonment rate driven by UX issues will not move because the underlying transactions started routing more intelligently.

It does not remove all risk of a payments incident. A well-architected orchestrator reduces single-points-of-failure dramatically, but it introduces one new dependency. If the orchestration platform itself goes down, every connected provider becomes inaccessible at once. The mitigation is at the architecture level, and it is one of the reasons the multi-tenant versus dedicated instance question matters. A platform built on dedicated cloud instances per customer has a much smaller blast radius than a multi-tenant platform where one incident affects every customer simultaneously.

The trade-offs are real, but they are also manageable. Merchants who implement payment orchestration with clear-eyed expectations about what it does and does not do consistently capture more of the available upside than merchants who treat it as a one-time fix.

Multi-tenant vs dedicated instance: the architecture trade-off most buyers miss

Two payment orchestration platforms can offer the same features and run on very different infrastructure. The distinction matters in 2026, particularly for merchants in regulated industries or markets with strict data residency requirements.

Multi-tenant payment orchestration runs on shared infrastructure across the platform’s customers. One set of servers, databases, and APIs serves all merchants. The benefits are speed and cost. The trade-off appears under specific conditions: traffic spikes from one merchant can affect performance for others, data sovereignty cannot be fully guaranteed, and the platform’s blast radius covers every customer at once.

Dedicated instance payment orchestration runs each customer on its own isolated cloud environment. Gr4vy is the only payment orchestration platform built this way. Each merchant’s orchestration layer, Vault, dashboard, and routing logic runs on infrastructure that nobody else shares. Data residency can be guaranteed by region. Performance does not depend on other tenants. The blast radius shrinks dramatically.

For enterprises in financial services, healthcare, regulated sectors, or any business where data sovereignty is a board-level concern, dedicated instance is often the requirement that disqualifies multi-tenant platforms outright.

How much does payment orchestration cost?

Pricing varies by platform and is typically based on processed volume, with custom enterprise pricing above certain thresholds. Most payment orchestration platforms add a per-transaction or platform fee on top of existing PSP fees.

At Gr4vy, pricing is tied to infrastructure rather than transaction volume alone, reflecting our Infrastructure-as-a-Service and single-tenant architecture. Every merchant operates on its own dedicated orchestration instance, with isolated infrastructure designed for greater control, resiliency, security, and regulatory flexibility. This model aligns our platform with the operational realities of enterprise payments, where infrastructure ownership, performance, and compliance are critical business requirements rather than shared SaaS resources.

At scale, the fee is offset by authorization-rate uplift, processing cost reductions, and reduced engineering overhead. The total cost of ownership of payment orchestration tends to fall, not rise, once it is in place. The Gr4vy ROI calculator gives a per-business estimate based on processed volume, current approval rates, and provider mix.

Is payment orchestration PCI compliant?

Yes, when the platform is properly certified. Look for PCI DSS Level 1, SOC 2 Type II, and ISO 27001. One of the secondary benefits of payment orchestration is that the merchant’s own PCI scope is reduced, because sensitive card data lives inside the platform’s tokenization Vault rather than across multiple systems.

Where payment orchestration is heading next

Payment orchestration began as a way to coordinate multiple integrations through a single API. The capabilities have grown well beyond that. Machine learning now optimizes routing decisions based on issuer response patterns the platform can detect across millions of transactions. Network Tokenization has moved from a card-network capability to a feature most payment orchestration platforms expose natively.

The most significant shift in the next two years is agentic commerce. AI agents are starting to initiate and complete purchases on behalf of consumers, often inside conversational interfaces like ChatGPT. The payments infrastructure required for agent-driven transactions differs from the infrastructure required for human checkouts. Gr4vy is the first payment orchestration platform to launch a dedicated Agentic Development Kit for this purpose, enabling its merchants to process agentic commerce payments.

Frequently asked questions

Is a payment orchestrator the same as a payment gateway?

No. A gateway transmits transaction data between the checkout and a processor. A payment orchestrator sits above gateways, PSPs, and acquirers, coordinating across all of them and providing a unified view of payment performance.

Is a payment orchestrator the same as a PSP?

No. A PSP processes payments and owns the merchant account. A payment orchestrator does not process payments. It decides which PSP should handle each transaction and can use multiple PSPs in parallel.

Do I need to replace my existing PSPs to use payment orchestration?

No. Payment orchestration sits on top of existing providers. PSP relationships, contracts, and merchant accounts stay in place. The platform coordinates how transactions flow across them.

How many providers do I need before payment orchestration makes sense?

Two or more is the practical threshold. The case for payment orchestration sharpens quickly as more providers are added.

Can payment orchestration help with recurring payments and subscriptions?

Yes. Centralized tokenization keeps recurring payments active when a merchant switches providers. Network Tokens, Account Updater, and dynamic retries recover the failed recurring charges that single-PSP setups lose to involuntary churn.

What is the difference between multi-tenant and dedicated instance payment orchestration?

Multi-tenant payment orchestration runs on shared infrastructure across all customers. Dedicated instance payment orchestration runs in a private cloud environment per customer. The trade-off is cost and time to deploy versus data sovereignty, blast-radius isolation, and configuration depth.

Payments have moved from a back-office cost line to one of the most consequential systems an online business operates. The merchants pulling away from their competition in 2026 are the ones treating it that way: measuring authorization rates the way they measure conversion, treating provider relationships as negotiable, and building the infrastructure to route transactions intelligently across multiple paths instead of accepting whatever a single PSP produces. Payment orchestration is the layer that makes that posture practical.

Gr4vy was built specifically for businesses ready to take that step. Talk to our team about your stack.