April 9, 2026

Payment methods by country 2026: what dominates each market and how to accept them

- Why payment method preference varies so much by country

- North America

- United States

- Canada

- Europe

- Germany

- Netherlands

- France

- Poland

- Nordic countries

- Asia-Pacific

- China

- India

- Japan

- Southeast Asia

- Latin America

- Brazil

- Mexico

- Middle East and Africa

- Saudi Arabia

- Kenya

- Payment methods by region: at a glance

- What this means for your payment stack

- Frequently asked questions

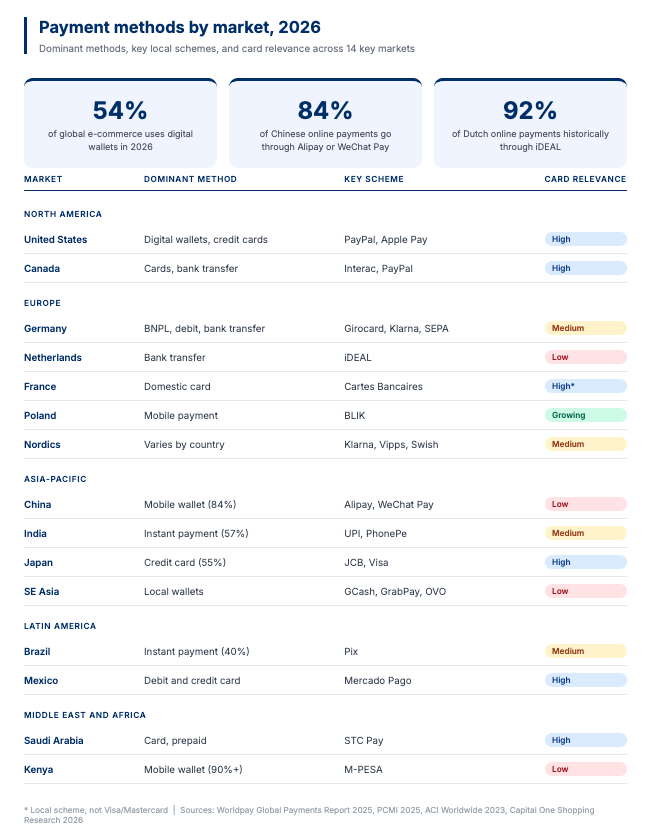

Offer the wrong payment method at checkout and the sale is already lost. According to Worldpay, digital wallets now account for 54% of e-commerce transactions globally in 2026, up from less than half just two years ago. That headline figure, though, tells merchants almost nothing useful. Japanese consumers pay online with credit cards 55% of the time.

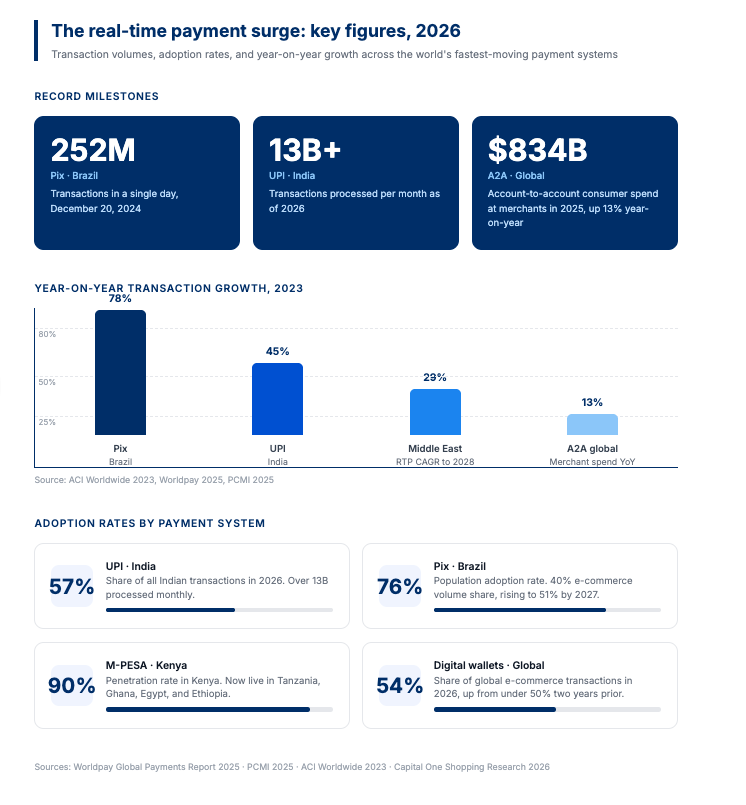

Dutch consumers expect iDEAL, a bank transfer scheme, so reliably that building a checkout without it guarantees abandonment. In Brazil, Pix, a government-built instant payment network, recorded 252 million transactions in a single day in December 2024 alone.

The practical question for any merchant selling across borders is which payment methods to support in which markets, and how to manage the operational weight of connecting to all of them. This guide works through the 12 most commercially significant markets in 2026, with the data behind each and what it takes to accept these methods reliably.

Why payment method preference varies so much by country

Consumer payment habits are shaped by a mix of banking infrastructure, regulation, cultural trust in financial institutions, and the timing of fintech adoption. A country that built strong real-time banking rails before smartphone wallets took off tends to retain those rails as a default. A country that leapfrogged traditional banking through mobile technology tends to run on wallets. A country where consumer credit was historically mistrusted tends to prefer bank transfers or debit.

These habits are deeply embedded, and a one-size-fits-all payment setup will underperform in most markets because of them. Understanding how local payment methods differ from international card schemes is the starting point for building a checkout that converts globally.

North America

United States

Credit cards still account for 31% of US online purchases, but digital wallets have closed the gap fast, reaching 39% of online transactions and projected to hit 52% by 2030. PayPal has a 71% penetration rate among US adults, which makes it the dominant e-commerce wallet by some distance. Apple Pay and Google Pay doubled their adoption between 2020 and 2025 but remain secondary to PayPal for online checkout. BNPL has found its footing with younger shoppers through Affirm, Klarna, and Afterpay, particularly in electronics, fashion, and home goods.

Visa and Mastercard are the baseline. PayPal adds meaningful conversion on top of that, and BNPL is worth evaluating in any category where average order values are high enough to make installments attractive.

Canada

Canada follows a similar card-heavy pattern to the US, with Visa and Mastercard dominant across both e-commerce and in-store. Interac, Canada’s domestic debit network, is widely used for in-store and online bank transfers. PayPal is the leading digital wallet. BNPL adoption is growing but still behind US levels.

Europe

Europe is where payment fragmentation is most pronounced. Visa and Mastercard dominate in some markets and barely register in others. Merchants expanding across Europe without a market-by-market payment strategy typically leave conversion on the table.

Germany

Cash still accounted for 51% of all German in-store transactions in a 2023 study, a figure that surprises most merchants entering the market for the first time. The Girocard debit scheme has over 100 million cards in circulation, and in the first half of 2025 debit cards made up 31% of non-cash payments. Online, BNPL runs deeper in Germany than in most comparable economies because German consumers have a long-standing habit of paying by invoice after goods arrive, a practice rooted in local consumer law. Klarna and PayPal are the methods that drive online volume. SEPA bank transfers handle B2B and recurring transactions. Card-only acceptance leaves a significant portion of the German market unreachable.

Netherlands

The Netherlands runs largely on iDEAL, a bank-initiated transfer scheme that historically captured around 92% of online payments. iDEAL is now migrating to a new version built on open banking infrastructure, but it remains the default for Dutch consumers at checkout. Credit card use is comparatively low. Any merchant launching in the Netherlands without iDEAL will see immediate checkout abandonment.

France

France has its own domestic card scheme, Cartes Bancaires, which processes the majority of card transactions. It coexists with Visa and Mastercard but operates on different rails and has different cost structures. PayPal is widely used online. For merchants, integrating Cartes Bancaires is not optional in France; it is the baseline.

Poland

Poland has become one of Europe’s more interesting payment markets. BLIK, a mobile payment method linked to bank accounts, processed over 420 million transactions in 2024 and has expanded into neighboring countries. Poland is also projected to be the fastest-growing country in the European payments market through 2031, at a CAGR of 15.05%. Card acceptance is growing, but BLIK is the preferred method for a large portion of the online population.

Nordic countries

Swish in Sweden, Vipps in Norway, MobilePay in Denmark, and online banking in Finland each lead their respective markets, and the overlap between them is smaller than the geography suggests. BNPL accounts for 23% of Swedish online transactions, driven by Klarna’s home-market strength. Danish consumers lean toward credit and debit cards at 52% of transactions. Finnish consumers default to online banking at 30%. A Nordic payment strategy that treats these four countries as a single market will get the mix wrong in at least three of them.

For a full breakdown of how regional compliance affects your payment setup, read our guide to payment orchestration in Europe.

Asia-Pacific

China

Alipay and WeChat Pay together account for 84% of Chinese online payments, with QR code transactions the norm in physical stores. Visa and Mastercard have negligible domestic penetration; UnionPay is the card network that actually matters. For international merchants selling into China, integrating Alipay and WeChat Pay through a compliant local partner is the only practical path to reaching Chinese consumers at checkout.

India

India’s UPI (Unified Payments Interface) is one of the most significant payment infrastructure stories of the decade. According to a 2026 study, UPI now accounts for 57% of transactions throughout India, with the system processing over 13 billion transactions per month. It contributed 55% to e-commerce volume in 2024 according to PCMI data. PhonePe and Google Pay are the largest UPI apps by volume. Credit and debit card acceptance matters for higher-value and international transactions, but any merchant selling in India without UPI integration is working around the country’s primary payment rail.

Japan

Japan is one of the few major markets where credit cards still dominate online payments at 55%, the highest rate of any country globally. This reflects both high credit card penetration and strong consumer trust in card-based transactions. Digital wallets are growing, but the credit card remains the default for Japanese online shoppers. In-store, QR code payments and IC card-based transit payments like Suica are common, but for e-commerce, card acceptance is the priority.

Southeast Asia

Southeast Asia rewards market-specific research rather than regional generalizations. GCash handles the bulk of digital payments in the Philippines. GrabPay and Touch ‘n Go lead in Malaysia. Dana and OVO are the dominant wallets in Indonesia. BNPL is growing across all three, and mobile-first infrastructure means local wallets carry more transaction volume than global card schemes in most of these markets.

Latin America

Brazil

Pix is Brazil’s payment story in 2026. The government-backed instant payment system has 76.4% adoption across Brazil’s 211 million people, commands a 40% e-commerce volume share according to PCMI data, and set a single-day record of 252.1 million transactions on December 20, 2024. By 2027, PCMI projects that share reaching 51%. Debit cards rank second in overall usage, and credit cards remain relevant for installment purchases, which Brazilian consumers use heavily given the country’s high credit card interest rates. Cash has dropped below 20% in urban areas but persists in rural markets.

Pix also carries lower transaction costs than card networks, which has a direct impact when cutting payment processing costs at scale.

Mexico

Mexico is still primarily card and cash-driven, with debit and credit cards the preferred methods for online purchases as of 2024. Cash remains the most used in-store payment method, though its share has been declining consistently since 2017. Digital wallets are growing, with mobile wallet market share rising from 4% in 2017 to 12% in 2023, driven largely by Mercado Pago.

Middle East and Africa

Saudi Arabia

Saudi Arabia has been transitioning from cash to digital payments faster than most markets in the region. Credit cards led online at 41% in 2021, and that share has continued to grow as card infrastructure matures. STC Pay and other local wallets are gaining ground. The country is also one of the highest users of debit and prepaid cards globally, at 33% of online transactions.

Kenya

Kenya’s M-PESA has over 90% penetration in its home market and has expanded to multiple African countries including Tanzania, Mozambique, Ghana, Egypt, and Ethiopia. In February 2025, Kenya ranked as the country with the highest digital payment adoption, with 80% of its population using digital payments. For merchants entering the Kenyan market, M-PESA integration is the single most important payment decision. Card acceptance matters for tourist-facing and international commerce, but domestic transactions run on M-PESA.

Payment methods by region: at a glance

| Region | Dominant method | Key local schemes | Card relevance |

| United States | Digital wallets, credit cards | PayPal, Apple Pay | High |

| Germany | BNPL, debit, bank transfer | Girocard, Klarna, SEPA | Medium |

| Netherlands | Bank transfer | iDEAL | Low |

| France | Domestic card | Cartes Bancaires | High (local scheme) |

| Poland | Mobile payment | BLIK | Medium and growing |

| China | Mobile wallet | Alipay, WeChat Pay | Very low (domestic) |

| India | Instant payment | UPI, PhonePe | Medium |

| Japan | Credit card | JCB, Visa | High |

| Brazil | Instant payment | Pix | Medium |

| Mexico | Debit and credit card | Mercado Pago | High |

| Saudi Arabia | Card, prepaid | STC Pay | High |

| Kenya | Mobile wallet | M-PESA | Low |

What this means for your payment stack

Supporting 12 different payment methods across 12 markets touches every layer of your payment stack: routing logic, reconciliation, compliance, and the checkout experience itself.

The merchants doing this well in 2026 are using a payment orchestration layer that connects to local payment methods through a single API, routes transactions based on availability and performance, and makes it possible to turn new methods on or off without engineering work.

For the payment method layer to work well, the checkout layer also needs to surface the right options to the right customers based on location and device. A German customer should see Klarna and SEPA. A Dutch customer should see iDEAL. A Brazilian customer should see Pix. Showing all methods to all customers hurts conversion. A checkout built to convert handles this dynamically, not through static configuration.

This is also where approval rate optimization becomes relevant. Even when you offer the right method, routing decisions determine whether the transaction succeeds. Read more about how to increase payment approval rates in 2026 through smarter routing and fallback logic.

The cost dimension matters too. Local payment methods like Pix, iDEAL, and UPI typically carry lower transaction fees than international card networks. The hidden costs in your payment stack shows how to quantify what you save by routing to the right method in each market.

Frequently asked questions

What is the most widely used payment method globally in 2026?

Digital wallets account for 54% of global e-commerce transactions in 2026, making them the single largest category. The leading wallet varies significantly by market. Alipay leads in China, UPI apps lead in India, PayPal leads in the US and much of Europe, and M-PESA leads in Kenya.

Do I need to support local payment methods or is card acceptance enough?

In most high-growth markets, card acceptance alone is not enough. In Brazil, Pix handles 40% of e-commerce volume. In the Netherlands, iDEAL has historically dominated with around 92% of online payments. In Germany, a significant share of consumers prefer BNPL or bank transfer online. Relying only on Visa and Mastercard will cost you real conversion in these markets.

How do I add local payment methods without rebuilding my integration?

Payment orchestration platforms connect to local payment methods through a single API and a no-code rules interface. Instead of integrating each scheme individually, you connect once and configure which methods appear in which markets. Read more about what a payment orchestrator does and what capabilities it covers.

Which markets have the most complex payment requirements?

China, India, Germany, and Brazil each require market-specific methods that sit outside standard card rails. Europe as a whole adds regulatory complexity through PSD2 and PSD3 and regional compliance requirements. Our guide to payment regulations across different regions in 2026 covers what merchants need to know.

What is the fastest-growing payment method by region?

Real-time account-to-account payments are growing fastest. India’s UPI grew 45% in 2023, Brazil’s Pix grew 78% in the same period, and Poland’s BLIK processed over 420 million transactions in 2024. Account-to-account consumer spending at merchants reached $834 billion globally in 2025, a 13% year-on-year increase.

How do I handle stored card data when expanding to new markets?

When you add new processors or PSPs to support local payment methods, stored card data needs to move with you. How to migrate stored card data between payment providers covers the process without disrupting existing customer relationships.

The numbers from 2026 make the case plainly. UPI processes 13 billion transactions a month in India. Pix broke 252 million transactions in a single day in Brazil. BLIK has crossed into multiple Central European markets. Digital wallets take 54% of global e-commerce volume. A decade ago, none of these methods existed at meaningful scale. Today, each one determines whether a checkout converts or abandons in its home market. The merchants doing this well have infrastructure flexible enough to add, route, and optimize payment methods without constant engineering involvement.

See how payment orchestration works with your existing processors and what it takes to go live in a new market. Book a demo.