September 18, 2025

What are the most popular alternative payment methods in Europe?

Alternative payment methods (APMs) are no longer optional in European ecommerce. Consumers across the region increasingly choose wallets, bank transfers, and local payment schemes over traditional cards. For merchants, ignoring these methods means lost revenue and lower conversion rates.

APMs are also closely tied to compliance. PSD2, GDPR, and national rules govern authentication, data handling, and customer rights. Merchants expanding across Europe must integrate APMs in ways that respect both consumer preferences and regulatory requirements.

This article explains the growth of APMs in Europe, outlines country-level adoption, and highlights how orchestration simplifies integration across diverse markets.

Growth of alternative payment methods

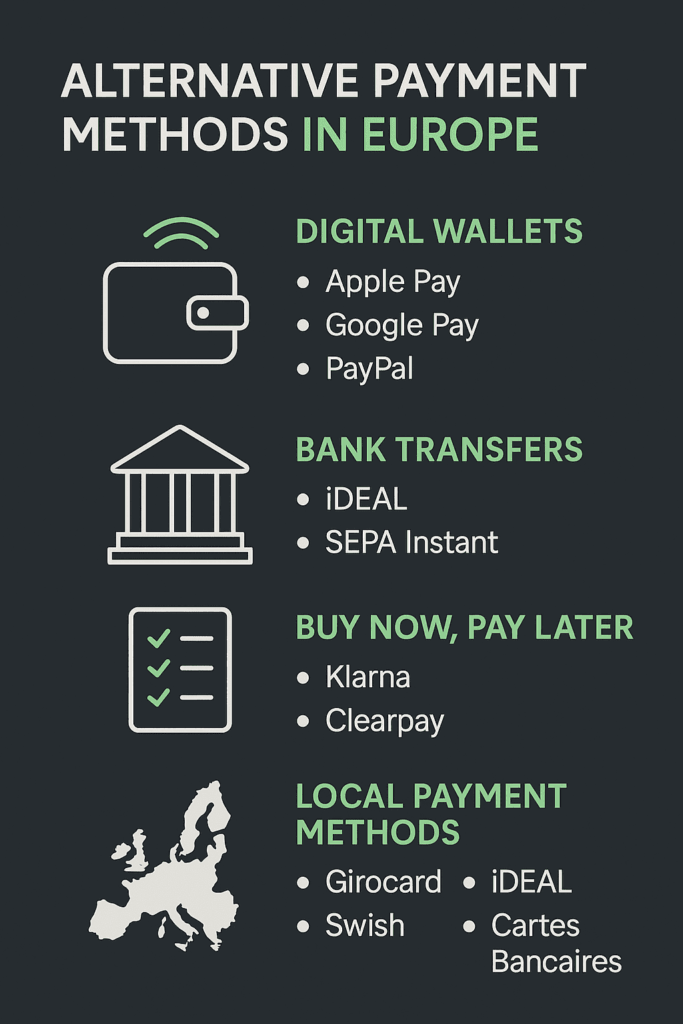

Ecommerce in Europe is shaped by diversity. While cards remain dominant in some regions, APMs are taking a larger share of online payments each year.

- Wallets like PayPal, Apple Pay, and Google Pay are mainstream across most markets.

- Bank-to-bank transfers are accelerating with SEPA Instant and open banking APIs.

- National schemes continue to dominate local markets, such as iDEAL in the Netherlands and Girocard in Germany.

Data from 50 payment and merchant statistics shaping Europe in 2025 shows that more than 60% of online shoppers now expect multiple APMs at checkout. Merchants that support them see higher approval rates and lower cart abandonment.

Country-level breakdown of APMs

Germany

German consumers prefer direct debit and local cards. Girocard, often co-badged with debit schemes, remains widely used. PayPal also has significant adoption in ecommerce.

Netherlands

iDEAL dominates Dutch ecommerce. More than 70% of online transactions flow through this bank-based method. Merchants entering this market must support iDEAL to compete effectively.

Nordics

Sweden’s Swish and Denmark’s MobilePay are leading mobile-first methods. Both are integrated into daily life and used for recurring as well as one-off payments.

France

Cartes Bancaires remains the national card network, but PayLib and wallets are gaining ground. Merchants must often support both cards and wallet-based flows.

UK

The UK combines card-on-file payments with newer options like Faster Payments and wallets. Buy Now Pay Later services have also gained strong traction.

Our guide to top payment methods in Europe explores these local preferences in greater detail and shows why localization is critical.

Wallets and digital-first methods

Wallet adoption continues to grow across Europe. Apple Pay and Google Pay are built into mobile devices, making them easy for consumers to use. PayPal remains a trusted brand, especially in cross-border transactions. Buy Now Pay Later providers like Klarna are reshaping ecommerce for younger demographics.

The European Payments Initiative is also rolling out Wero, a digital wallet designed to compete with global providers and standardize payments across EU countries. For merchants, Wero signals the increasing importance of EU-backed solutions.

For a broader overview of how wallets are changing checkout behavior, see our report on digital wallets in Europe.

Bank-to-bank rails and open banking

Open banking APIs, combined with SEPA Instant, are creating account-to-account (A2A) payment flows that bypass cards entirely. These methods allow merchants to accept payments directly from customer accounts with lower fees and faster settlement.

The EU Instant Payments Regulation, which requires banks to support SEPA Instant, will further accelerate adoption. This will bring APMs closer to real-time status and reduce reliance on traditional card infrastructure.

More details are covered in our guide on real-time payments across Europe.

Compliance and security considerations

Adopting alternative payment methods requires merchants to meet strict compliance standards:

- PSD2 and SCA: Strong Customer Authentication applies to most APMs, including wallets and open banking flows. Merchants must ensure exemptions are applied correctly to avoid declined payments.

- GDPR: Wallets and account-to-account payments involve storing and processing sensitive data. Customers must have transparency and control over how their data is used.

- AML and KYC: For bank-to-bank and direct debit payments, merchants must align with anti-money laundering rules. This is especially relevant for platforms that process payments on behalf of multiple sellers.

- Refunds and disputes: National rules, such as SEPA Direct Debit’s refund framework, affect how disputes are handled and what liability merchants face.

For more detail on regulatory frameworks, see our guide to embedded payments compliance in Europe.

Why orchestration is key for APM integration

Supporting APMs across multiple European countries without orchestration is complex and costly. Each method has its own technical requirements, compliance checks, and reporting standards. Payment orchestration simplifies this through a single control layer:

- Unified access: One integration unlocks multiple APMs, from iDEAL to Swish.

- Dynamic routing: Merchants can prioritize local methods where they perform best.

- Scalability: Adding new APMs does not require new one-off integrations.

- Centralized compliance: Fraud checks, SCA flows, and reporting can be managed in one place.

For merchants expanding into multiple EU markets, orchestration provides the flexibility and resilience that a single PSP cannot. See our analysis on why payment orchestration matters for European merchants expanding cross-border for more.

Roadmap for merchants

Merchants looking to implement APMs effectively should:

- Research market preferences: Identify which APMs dominate in each target country. Top payment methods in Europe is a useful starting point.

- Prioritize compliance: Map how PSD2, GDPR, and AML apply to each payment flow.

- Adopt orchestration: Use a single layer to integrate, route, and monitor APMs across borders.

- Optimize checkout UX: Present local APMs clearly, ensuring they are trusted and familiar to customers.

- Monitor performance data: Track approval rates, dispute levels, and adoption to refine the mix of APMs offered.

FAQ

What are the most popular alternative payment methods in Europe?

iDEAL in the Netherlands, Girocard and PayPal in Germany, Swish and MobilePay in the Nordics, and wallets like Apple Pay and Google Pay across many markets.

Is iDEAL only for Dutch customers?

Yes, iDEAL is specific to the Netherlands, but it sets an example of how strong national APMs can dominate local ecommerce.

How do SEPA Instant and open banking affect APM adoption?

They accelerate account-to-account payments, offering faster and lower-cost alternatives to cards.

Are APMs more secure than cards?

They often offer equal or higher security due to real-time bank authentication and strong encryption. Compliance with PSD2 makes them robust.

Can orchestration handle multiple APMs at once?

Yes. Orchestration allows merchants to integrate and manage multiple APMs across countries through one unified platform.

Alternative payment methods are shaping the future of European ecommerce. Consumers increasingly expect to pay with wallets, bank transfers, or trusted local schemes, not just cards.

Merchants that adapt to these expectations improve conversion, strengthen customer trust, and expand more effectively across borders. Orchestration is the most efficient way to integrate and manage APMs at scale, while meeting compliance requirements and reducing operational complexity.

Contact Gr4vy to streamline alternative payment method integration and build a checkout strategy that fits every European market.